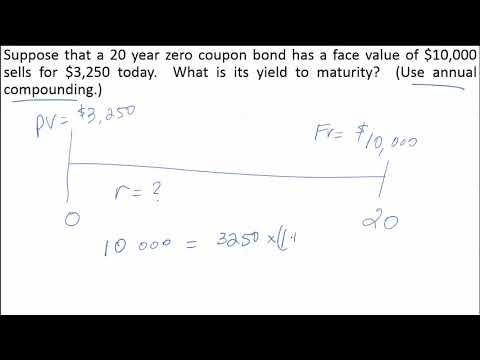

38 yield to maturity of a zero coupon bond

Zero Coupon Bond Calculator - What is the Market Price? - DQYDJ So a 10 year zero coupon bond paying 10% interest with a $1000 face value would cost you $385.54 today. In the opposite direction, you can compute the yield to maturity of a zero coupon bond with a regular YTM calculator. Other Financial Basics Calculators Zero coupon bonds are yet another interesting security in the fixed income world. Bond Yield to Maturity (YTM) Calculator - DQYDJ This makes calculating the yield to maturity of a zero coupon bond straight-forward: Let's take the following bond as an example: Current Price: $600. Par Value: $1000. Years to Maturity: 3. Annual Coupon Rate: 0%. Coupon Frequency: 0x a Year. Price =. (Present Value / Face Value) ^ (1/n) - 1 =.

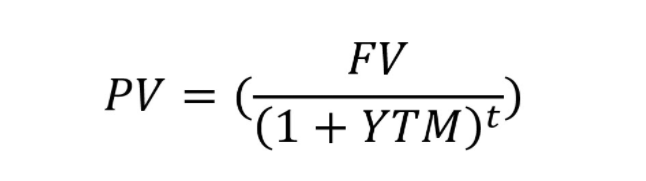

Value and Yield of a Zero-Coupon Bond | Formula & Example - XPLAIND.com The bonds were issued at a yield of 7.18%. The forecasted yield on the bonds as at 31 December 20X3 is 6.8%. Find the value of the zero-coupon bond as at 31 December 2013 and Andrews expected income for the financial year 20X3 from the bonds. Value (31 Dec 20X3) =. $1,000. = $553.17. (1 + 6.8%) 9. Value of Total Holding = 100 × $553.17 ...

Yield to maturity of a zero coupon bond

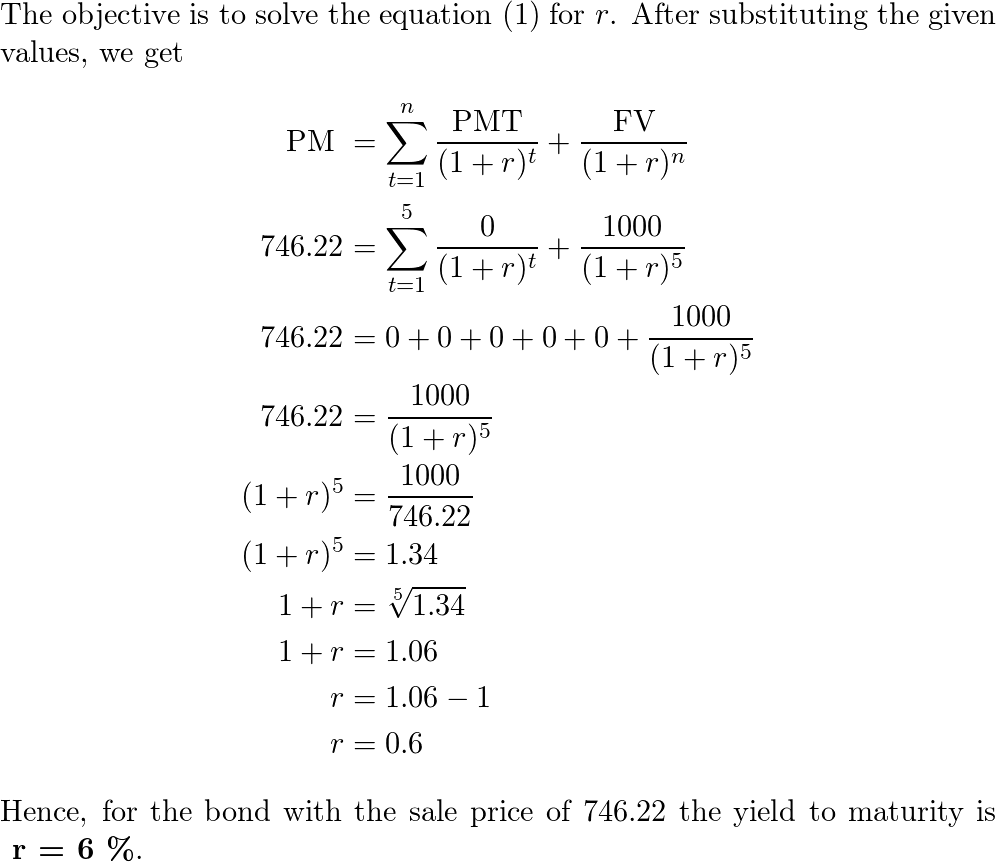

The yield to maturity on 1-year zero-coupon bonds is | Chegg.com Expert Answer. The yield to maturity on 1-year zero-coupon bonds is currently 8\%; the YTM on 2-year zeros is 9%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 10%. The face value of the bond is $100. a. Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Calculating Yield to Maturity on a Zero-coupon Bond YTM = (M/P) 1/n - 1 variable definitions: YTM = yield to maturity, as a decimal (multiply it by 100 to convert it to percent) M = maturity value P = price n = years until maturity Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Yield Curves for Zero-Coupon Bonds - Bank of Canada These files contain daily yields curves for zero-coupon bonds, generated using pricing data for Government of Canada bonds and treasury bills. Each row is a single zero-coupon yield curve, with terms to maturity ranging from 0.25 years (column 1) to 30.00 years (column 120). The data are expressed as decimals (e.g. 0.0500 = 5.00% yield). A ...

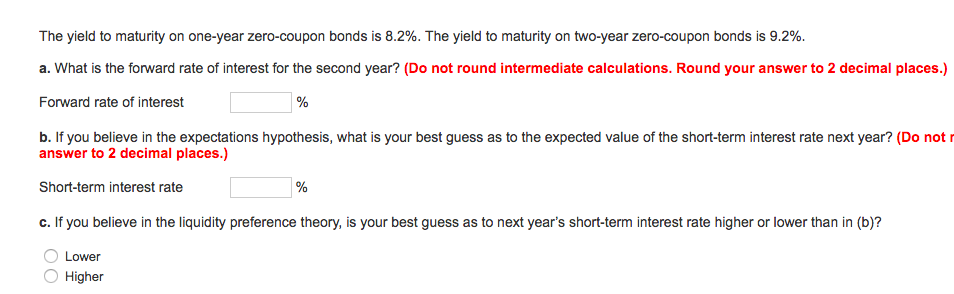

Yield to maturity of a zero coupon bond. Zero Coupon Bond | Investor.gov The maturity dates on zero coupon bonds are usually long-term—many don't mature for ten, fifteen, or more years. These long-term maturity dates allow an investor to plan for a long-range goal, such as paying for a child's college education. With the deep discount, an investor can put up a small amount of money that can grow over many years. Solved The yield to maturity on one-year zero-coupon bonds | Chegg.com The yield to maturity on one-year zero-coupon bonds is 8.4%. The yield to maturity on two-year zero-coupon bonds is 9.4%. a. What is the forward rate of interest for the second year? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Forward rate of interest % b. If you believe in the expectations hypothesis ... Zero Coupon Bond Value - Formula (with Calculator) - finance formulas A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value. Zero Coupon Bond Calculator 【Yield & Formula】 - Nerd Counter For instance, the maturity period of a zero-coupon bond is 10-years, its par value is $1000, the interest rate is 5.00%. When we are calculating the bond price in Excel, suppose we use the B column of the excel sheet for entering the values where B2 is the face value, B3 is the maturity time period, B4 is the interest rate.

Return of zero coupon bond. Yield to Maturity of zero coupon bond Learn how to calculate effective annual rate of zero coupon bond using formula approach. @RK varsity How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping As the face value paid at the maturity date remains the same (1,000), the price investors are willing to pay to buy the zero coupon bonds must fall from 816 to 751, in order from the return to increase from 7% to 10%. Bond Price and Term to Maturity The longer the term the zero coupon bond is issued for the lower the bond price will be. Bonds Flashcards | Quizlet A zero-coupon bond has a yield to maturity of 9% and a par value of $1,000. If the bond matures in eight years, the bond should sell for a price of _____ today. ... a 15-year zero-coupon bond that has a par value of $1,000, and a required return of 8% would be priced at approximately A. $308. B. $315. C. $464. D. $555. E. None of the options Important Differences Between Coupon and Yield to Maturity - The Balance The yield increases from 2% to 4%, which means that the bond's price must fall. Keep in mind that the coupon is always 2% ($20 divided by $1,000). That doesn't change, and the bond will always payout that same $20 per year. But when the price falls from $1,000 to $500, the $20 payout becomes a 4% yield ($20 divided by $500 gives us 4%).

Zero Coupon Bond Yield - Formula (with Calculator) - finance formulas The formula for calculating the effective yield on a discount bond, or zero coupon bond, can be found by rearranging the present value of a zero coupon bond formula: This formula can be written as This formula will then become By subtracting 1 from the both sides, the result would be the formula shown at the top of the page. Return to Top FINANCE - Module 7 Flashcards | Quizlet The yield to maturity for a zero-coupon bond is the return you will earn as an investor from holding the bond to maturity and receiving the promised face value payment. D. When prices are quoted in the bond market, they are conventionally quoted assuming the face value is $1000. E. Because we can convert any bond price into a yield, and vice ... Spot, Yield, Par and Forward Curves | CFA Level 1 - AnalystPrep Spot Curve, Yield Curve on Coupon Bonds, Par Curve, and Forward Curve. 27 Sep 2019. Yields-to-maturity for zero-coupon government bonds could be analyzed for a full range of maturities called the government bond spot curve (or zero curve). Government spot rates are assumed to be risk-free. Yield to maturity - Wikipedia Formula for yield to maturity for zero-coupon bonds = ... Suppose that over the first 10 years of the holding period, interest rates decline, and the yield-to-maturity on the bond falls to 7%. With 20 years remaining to maturity, the price of the bond will be 100/1.07 20, or $25.84. Even though the yield-to-maturity for the remaining life of ...

Understanding Interest Rates - ppt download

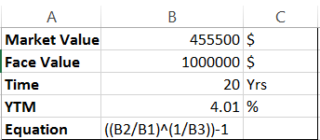

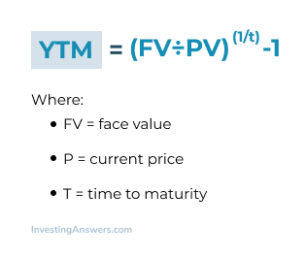

Zero-Coupon Bonds: Characteristics and Examples - Wall Street Prep To calculate the yield-to-maturity (YTM) on a zero-coupon bond, first divide the face value (FV) of the bond by the present value (PV). The result is then raised to the power of one divided by the number of compounding periods. Formula Yield-to-Maturity (YTM) = (FV / PV) ^ (1 / t) - 1 Interest Rate Risks and "Phantom Income" Taxes

VALUING BONDS

What Is a Zero-Coupon Bond? - Investopedia The interest earned on a zero-coupon bond is an imputed interest, meaning that it is an estimated interest rate for the bond and not an established interest rate. For example, a bond with a...

MGT338 - Chapter 6: Valuing Bonds | Team Study

Question : The current yield curve for default-free zero-coupon bonds ... Expert Answer 93% (15 ratings) 1. YTM = 10%, forward rate is not applicable, short rate = 10% Price = 1000/1+0.1 = 909.09 YTM = 11%, Forward rate = [ (1+YTM)^2 / (1+YTM0)]-1 = [ (1+0.11)^2 / … View the full answer Previous question Next question

How can I calculate the present value of a bond using YTM ...

Zero Coupon Bond - (Definition, Formula, Examples, Calculations) Cube Bank intends to subscribe to a 10-year this Bond having a face value of $1000 per bond. The Yield to Maturity is given as 8%. Accordingly, Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19.

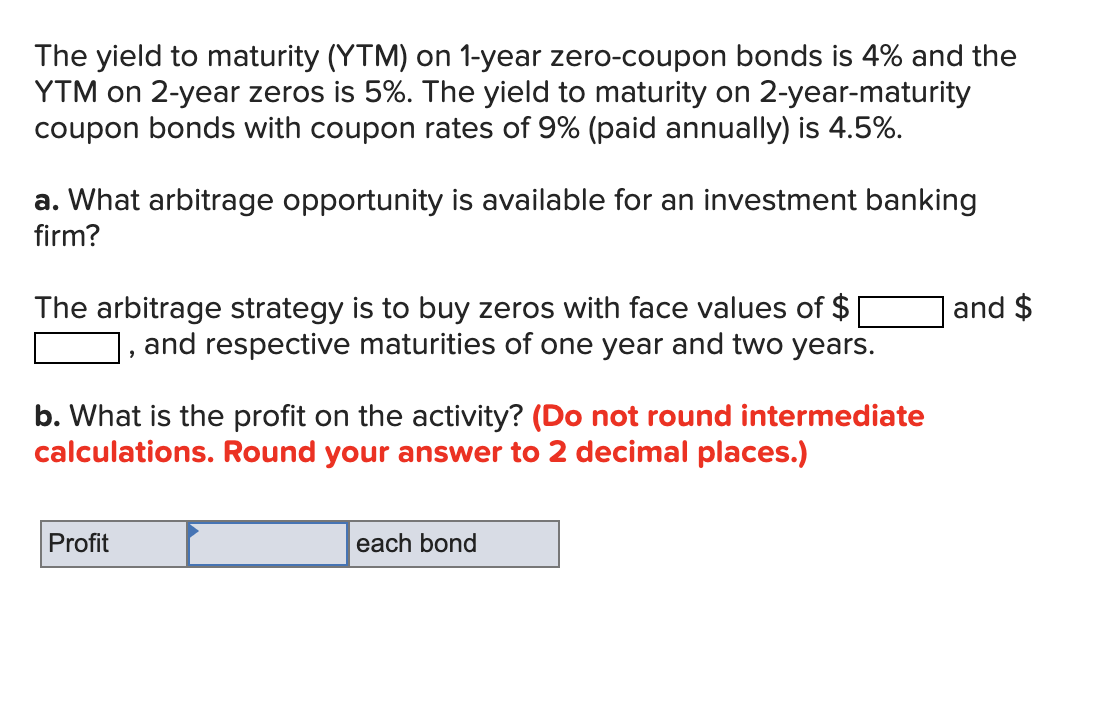

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5 ...

Understanding Coupon Rate and Yield to Maturity of Bonds Here's a sample computation for a Retail Treasury Bond issued by the Bureau of Treasury: Security Name. Coupon Rate. Maturity Date. RTB 03-11. 2.375%. 3/9/2024. The Coupon Rate is the interest rate that the bond pays annually, gross of applicable taxes. The frequency of payment depends on the type of fixed income security.

Zero-Coupon Bond - an overview | ScienceDirect Topics

How to Calculate Yield to Maturity of a Zero-Coupon Bond - Investopedia Yield to maturity is an essential investing concept used to compare bonds of different coupons and times until maturity. Without accounting for any interest payments, zero-coupon...

Zero-Coupon Bond - an overview | ScienceDirect Topics

Yield Curves for Zero-Coupon Bonds - Bank of Canada These files contain daily yields curves for zero-coupon bonds, generated using pricing data for Government of Canada bonds and treasury bills. Each row is a single zero-coupon yield curve, with terms to maturity ranging from 0.25 years (column 1) to 30.00 years (column 120). The data are expressed as decimals (e.g. 0.0500 = 5.00% yield). A ...

Solved] A 12.75-year maturity zero-coupon bond selling at a ...

Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Calculating Yield to Maturity on a Zero-coupon Bond YTM = (M/P) 1/n - 1 variable definitions: YTM = yield to maturity, as a decimal (multiply it by 100 to convert it to percent) M = maturity value P = price n = years until maturity Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years.

What is the yield to maturity (YTM) of a zero coupon bond ...

The yield to maturity on 1-year zero-coupon bonds is | Chegg.com Expert Answer. The yield to maturity on 1-year zero-coupon bonds is currently 8\%; the YTM on 2-year zeros is 9%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 10%. The face value of the bond is $100. a.

What is a Zero Coupon Bond? Who Should Invest? | Scripbox

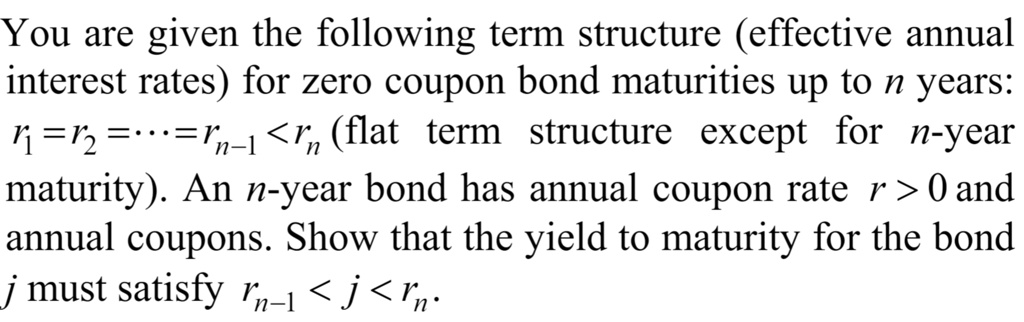

SOLVED: You are given the following term structure (effective ...

Computing Risk Free Rates and Excess Returns Part 1: From ...

Yield to Maturity – What it is, Use, & Formula – Speck & Company

The Dummies Guide To Zero Coupon Bonds

YIELDS TO MATURITY ON ZERO-COUPON RONDS

Zero Coupon Bonds Explained (With Examples) - Fervent ...

Zero Coupon Bond Valuation using Excel

Yield to Maturity (YTM) Definition & Example | InvestingAnswers

Zero Coupon Bonds

Zero Coupon Bonds Explained (With Examples) - Fervent ...

Learn to Calculate Yield to Maturity in MS Excel

PDF) Online Test 1 Answer Key | àOKF KDF - Academia.edu

Solved The yield to maturity on one-year zero-coupon bonds ...

A newly issued 20-year maturity, zero-coupon bond is issued ...

Solved] The yield to maturity on 1 year zero coupon bonds is ...

Explain conceptually how bonds are priced. Moreover, define ...

Trading zero-coupon bond with maturity T = 5 years. Average ...

A zero-coupon bond with face value $1,000 and maturity of fi ...

Solved The yield to maturity (YTM) on 1-year zero-coupon ...

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

LECTURE 09: MULTI-PERIOD MODEL BONDS

2: Value of Zero-Coupon Bond Against Yield to Maturity ...

Calculate the YTM of a Zero Coupon Bond

Yield to Maturity – What it is, Use, & Formula – Speck & Company

Zero-Coupon Bonds: Characteristics and Examples

Solved] Problem 15-7 The following is a list of prices for ...

1: Yield curves for Danish zero-coupon bonds. The red curve ...

Zero Coupon Bonds - Financial Edge

Post a Comment for "38 yield to maturity of a zero coupon bond"