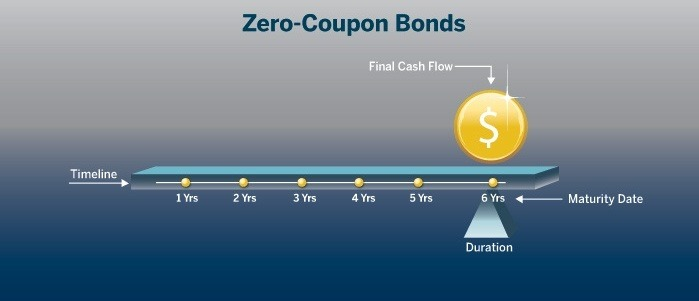

40 duration for zero coupon bond

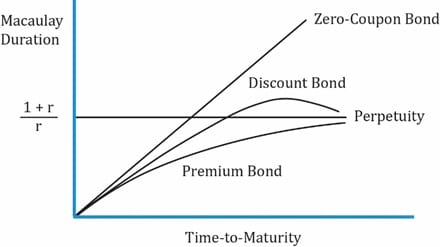

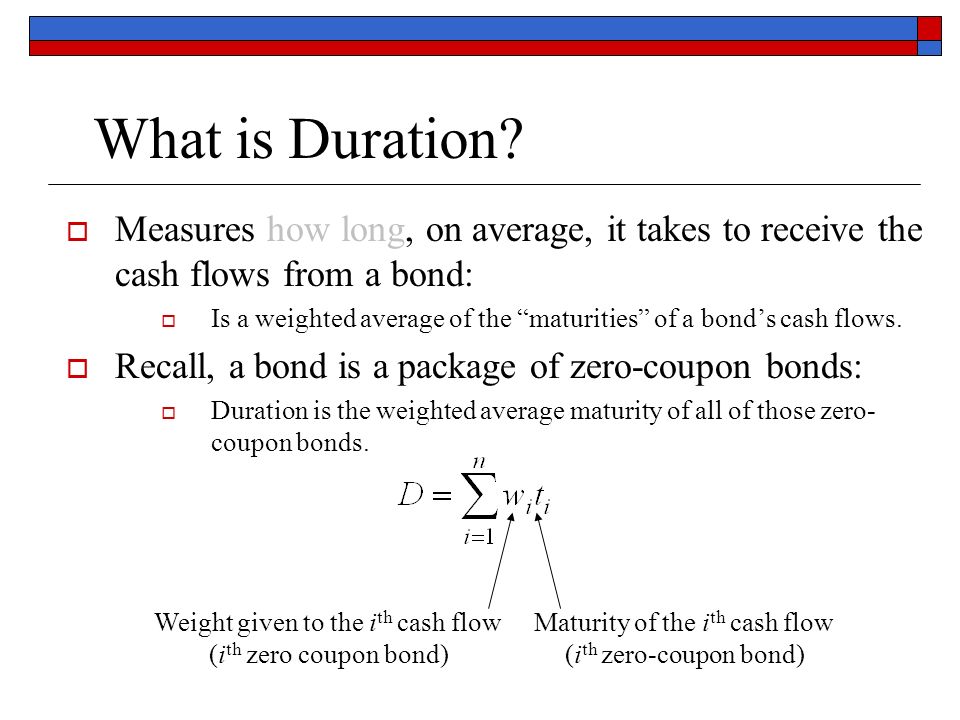

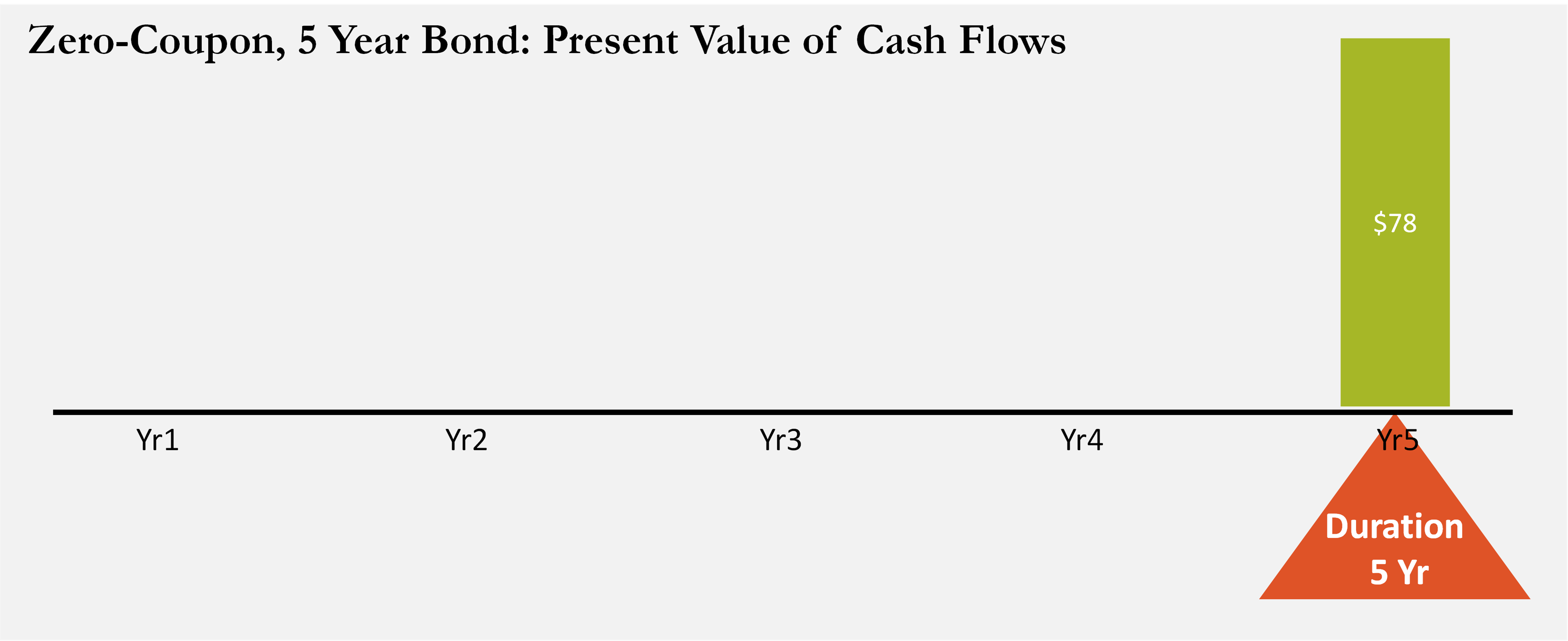

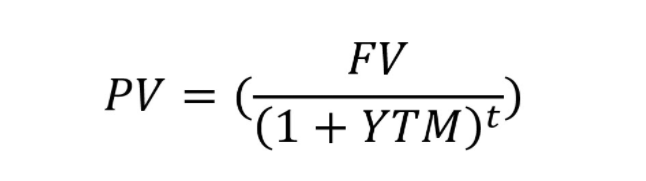

Duration: Understanding the Relationship Between Bond Prices and ... In the case of a zero-coupon bond, the bond's remaining time to its maturity date is equal to its duration. When a coupon is added to the bond, however, the bond's duration number will always be less than the maturity date. The larger the coupon, the shorter the duration number becomes. Generally, bonds with long maturities and low coupons have ... How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping n = 10 i = 7% FV = Face value of the bond = 1,000 Zero coupon bond price = FV / (1 + i) n Zero coupon bond price = 1,000 / (1 + 10%) 10 Zero coupon bond price = 508.35 (rounded to 508) In this example the bondholder has to wait 10 years before they receive the face value of the bond.

Convexity of a Bond | Formula | Duration | Calculation - WallStreetMojo The duration of the zero-coupon bond which is equal to its maturity (as there is only one cash flow) and hence its convexity is very high; While the duration of the zero-coupon bond Zero-coupon Bond In contrast to a typical coupon-bearing bond, a zero-coupon bond (also known as a Pure Discount Bond or Accrual Bond) is a bond that is issued at a ...

Duration for zero coupon bond

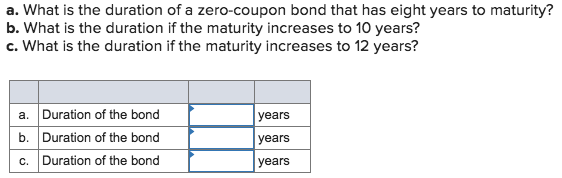

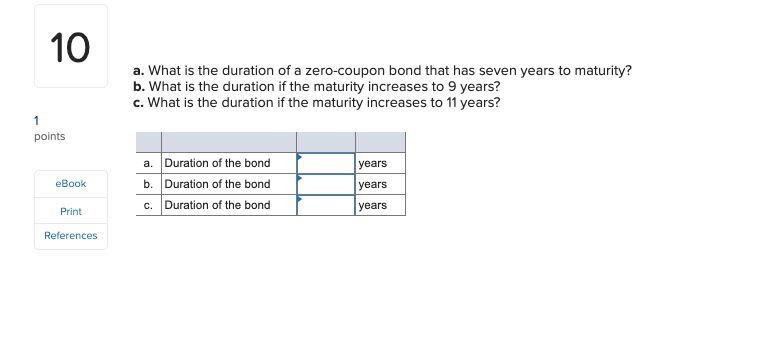

What is the duration of a zero-coupon bond that has eight years ... - Quora The duration of a zero-coupon bond is by definition equal to its maturity, so an 8-year zero has a duration of 8 years. If the maturity increases to 10 years, then so does the duration. 1 Kyle Taylor Founder at The Penny Hoarder (2010-present) Updated Wed Promoted Should you leave more than $1,000 in a checking account? You've done it. Modified Duration - Overview, Formula, How To Interpret Tim holds a 5-year bond with a face value of $1,000 and an annual coupon rate of 5%. The current rate of interest is 7%, and Tim would like to determine the Macaulay duration of the bond. The calculation is given below: The Macaulay duration for the 5-year bond is calculated as $4152.27 / $918.00 = 4.52 years. Putting it Together nerdcounter.com › zero-coupon-bond-calculatorZero Coupon Bond Calculator - Nerd Counter How to Calculate the Price of Zero Coupon Bond? The particular formula that is used for calculating zero coupon bond price is given below: P (1+r)t; Examples: Now come to a zero coupon bond example, if the face value is $2000 and the interest rate is 20%, we will calculate the price of a zero coupon bond that matures in 10 years.

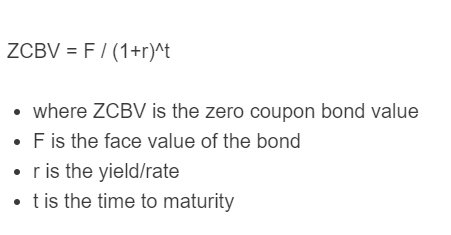

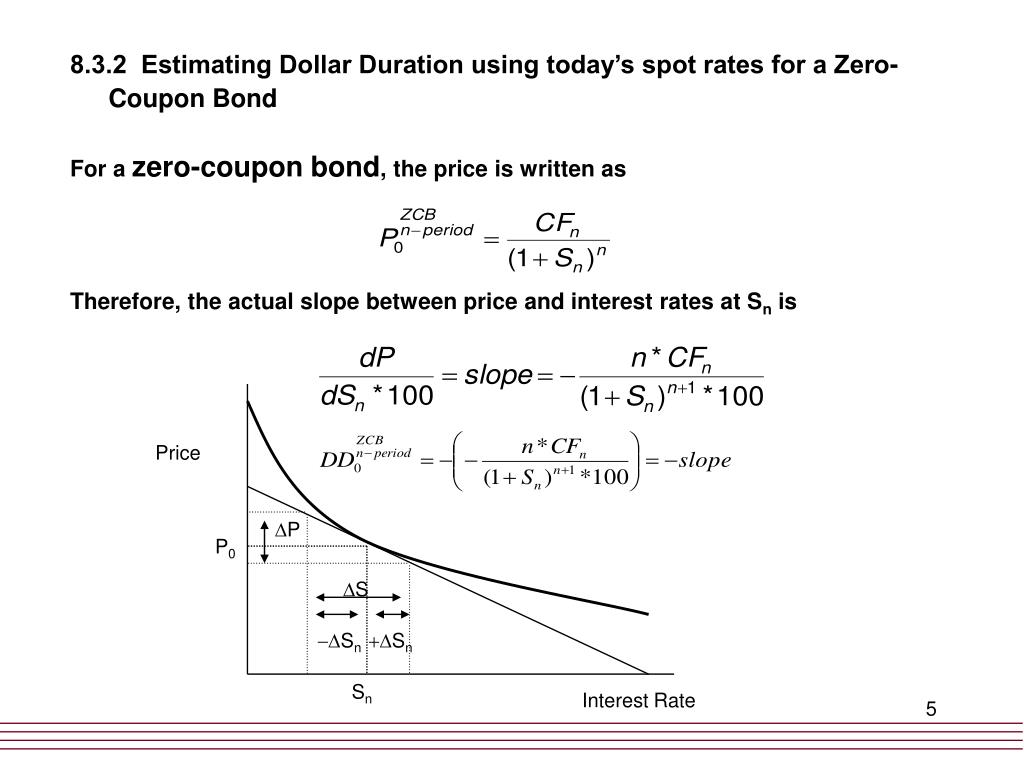

Duration for zero coupon bond. Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Divide the $1,000 by $500 gives us 2. Raise 2 to the 1/30th power and you get 1.02329. Subtract 1, and you have 0.02329, which is 2.3239%. Advantages of Zero-coupon Bonds Most bonds typically pay out a coupon every six months. Zero Coupon Bond Value - Formula (with Calculator) - finance formulas A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value. PDF Understanding Duration - BlackRock maturity. The higher a bond's coupon, the shorter its duration, because proportionately more payment is received before final maturity. • Because zero coupon bonds make no coupon payments, a zero coupon bond's duration will be equal to its maturity. • The longer a bond's maturity, the longer its duration, because it takes more time to receive full payment. The shorter a bond's maturity, the shorter its duration, What are Zero-Coupon Bonds? (Definition, Formula, Example, Advantages ... With zero-coupon bonds, the bondholders need to pay taxes associated with interest income, even though the particular gain has been realized or not. For example, with a bond that matures in 5 years, the lump sum return will only be generated at the end of the period. However, the bondholder must pay taxes, regardless of the time to maturity.

Zero Coupon Bond -Features, benefits, drawbacks, taxability ... - Fisdom Duration in a zero-coupon bond is the time to maturity. Normally, these bonds come with a duration of 10 years or more. How to invest in zero coupon bonds? Zero coupon bonds are issued periodically by governments and pseudo-government institutions. Once these bonds are issued, they can be bought through stock exchanges such as NSE and BSE. Zero Coupon Bond - (Definition, Formula, Examples, Calculations) Cube Bank intends to subscribe to a 10-year this Bond having a face value of $1000 per bond. The Yield to Maturity is given as 8%. Accordingly, Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. Zero-Coupon Bond - Definition, How It Works, Formula Interest rate risk is relevant when an investor decides to sell a bond before maturity and affects all types of fixed-income investments. For example, recall that John paid $783.53 for a zero-coupon bond with a face value of $1,000, 5 years to maturity, and a 5% interest rate compounded annually. Zero Coupon Bond | Investor.gov The maturity dates on zero coupon bonds are usually long-term—many don't mature for ten, fifteen, or more years. These long-term maturity dates allow an investor to plan for a long-range goal, such as paying for a child's college education. With the deep discount, an investor can put up a small amount of money that can grow over many years.

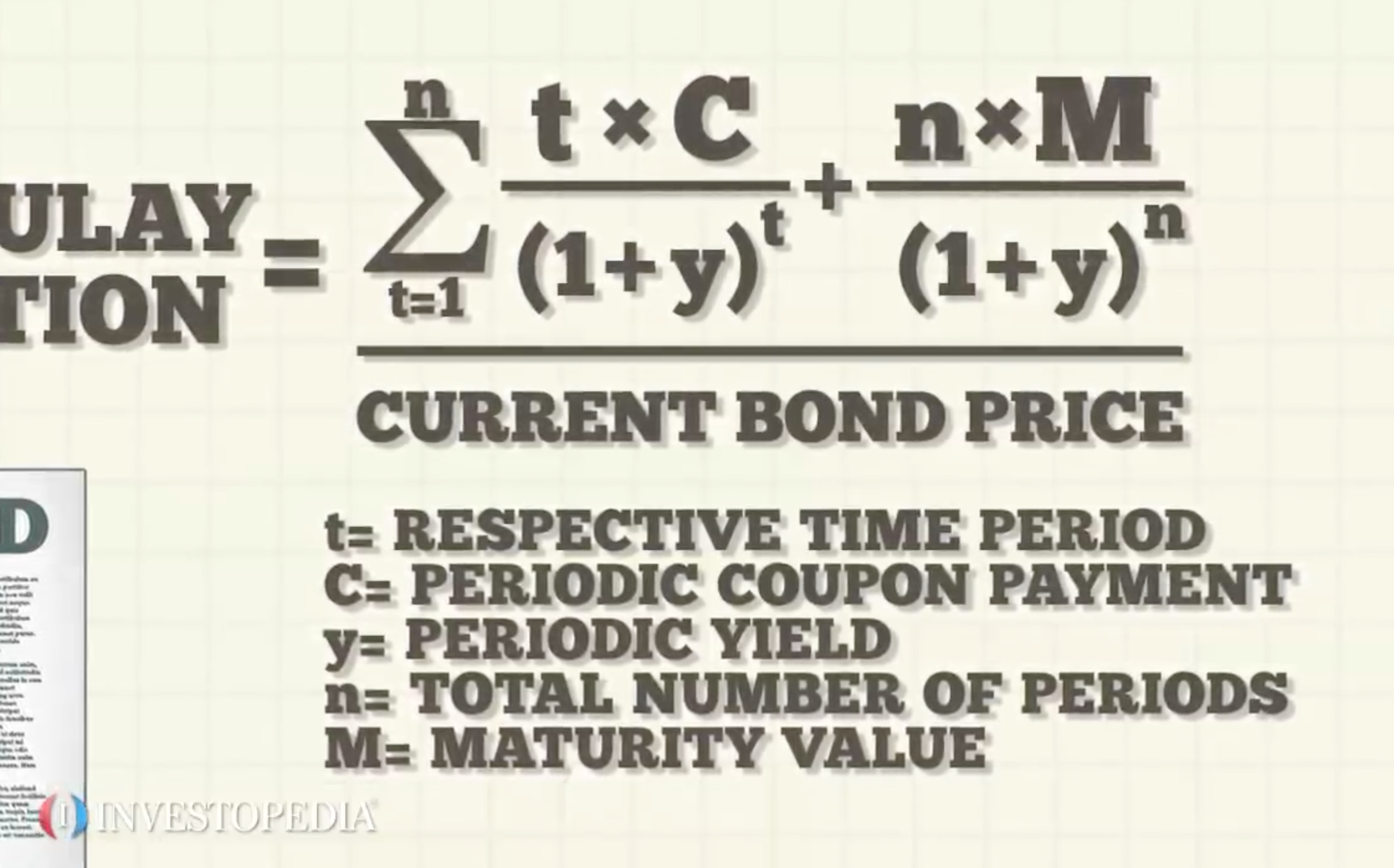

› investors › insightsThe One-Minute Guide to Zero Coupon Bonds | FINRA.org For example, you might pay $3,500 to purchase a 20-year zero coupon bond with a face value of $10,000. After 20 years, the issuer of the bond pays you $10,000. For this reason, zero coupon bonds are often purchased to meet a future expense such as college costs or an anticipated expenditure in retirement. Federal agencies, municipalities ... What is the duration of a zero coupon bond? - Quora Originally Answered: what is the duration of a zero coupon bond? Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium. nerdcounter.com › zero-coupon-bond-calculatorZero Coupon Bond Calculator - Nerd Counter How to Calculate the Price of Zero Coupon Bond? The particular formula that is used for calculating zero coupon bond price is given below: P (1+r)t; Examples: Now come to a zero coupon bond example, if the face value is $2000 and the interest rate is 20%, we will calculate the price of a zero coupon bond that matures in 10 years. Modified Duration - Overview, Formula, How To Interpret Tim holds a 5-year bond with a face value of $1,000 and an annual coupon rate of 5%. The current rate of interest is 7%, and Tim would like to determine the Macaulay duration of the bond. The calculation is given below: The Macaulay duration for the 5-year bond is calculated as $4152.27 / $918.00 = 4.52 years. Putting it Together

Zero Coupon Bond Calculator - Calculator Academy

What is the duration of a zero-coupon bond that has eight years ... - Quora The duration of a zero-coupon bond is by definition equal to its maturity, so an 8-year zero has a duration of 8 years. If the maturity increases to 10 years, then so does the duration. 1 Kyle Taylor Founder at The Penny Hoarder (2010-present) Updated Wed Promoted Should you leave more than $1,000 in a checking account? You've done it.

THE DURATION OF A BOND AS A PRICE ELASTICITY AND A FULCRUM

A default-free zero-coupon bond costs $91 and will pay $100 ...

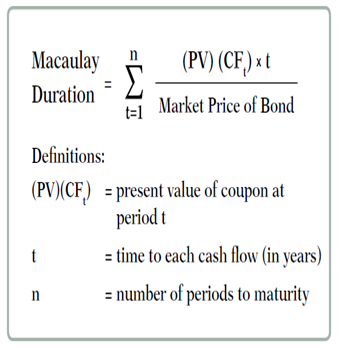

Macaulay Duration

Macaulay Duration

Understanding Fixed-Income Risk and Return | IFT World

PPT - 8. Measuring Interest Rate Risk-- Duration and ...

Modified Duration - Zero Coupon Bond Modified Duration ...

Bond duration - Wikipedia

Solved a. What is the duration of a zero-coupon bond that ...

SOLVED:Unvolve zero-coupon bonds. A zero-coupon bond is a ...

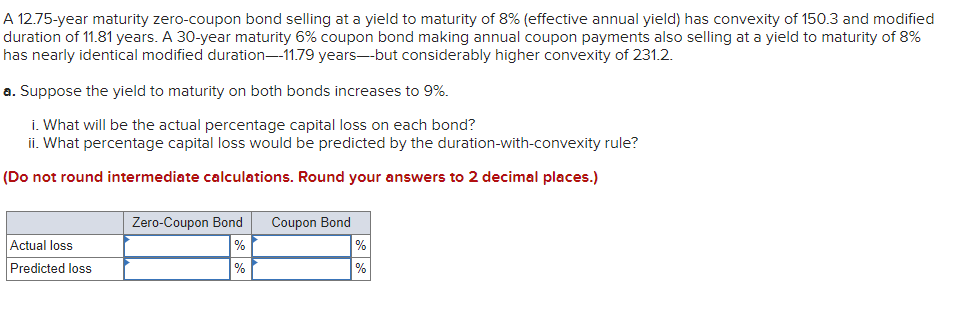

Solved A 12.75-year maturity zero-coupon bond selling at a ...

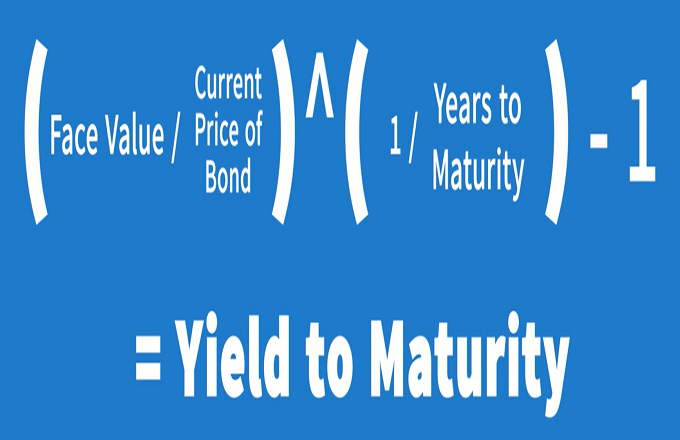

How Do I Calculate Yield To Maturity Of A Zero Coupon Bond?

![PDF] Duration and convexity of zero-coupon convertible bonds ...](https://d3i71xaburhd42.cloudfront.net/39b5487ce4f8becdfb0faf5ae6e30fd10537436c/13-Figure5-1.png)

PDF] Duration and convexity of zero-coupon convertible bonds ...

Modified duration of zero-coupond bond (FRM practice question)

:max_bytes(150000):strip_icc()/zero-couponbond_final-a6ec3618516a49c9a3654a1c79c9b681.png)

Zero-Coupon Bond: Definition, How It Works, and How To Calculate

Zero Coupon Bonds Explained (With Examples) - Fervent ...

How to Calculate PV of a Different Bond Type With Excel

Duration model

Macaulay's Duration, a Second Look - GlynHolton.com

Advanced Bond Concepts: Duration | The Financial Engineer

A 12.75-year maturity zero-coupon bond selling at a yield to ...

Investment Improvement: Adding Duration to the Toolbox | St ...

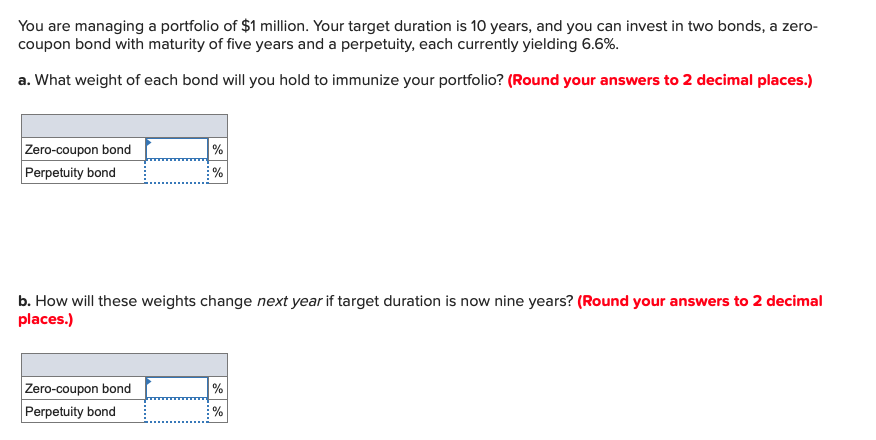

Solved You are managing a portfolio of $1 million. Your ...

Zero Coupon Bonds

Solved] You are managing a portfolio of $1.3 million. Your ...

Chapter 4 Bond Price Volatility Chapter Pages 58-85, ppt download

Bonds of Mass Destruction - The Last Bear Standing

THE RELATIONSHIP BETWEEN YIELD DURATION AND MATURITY

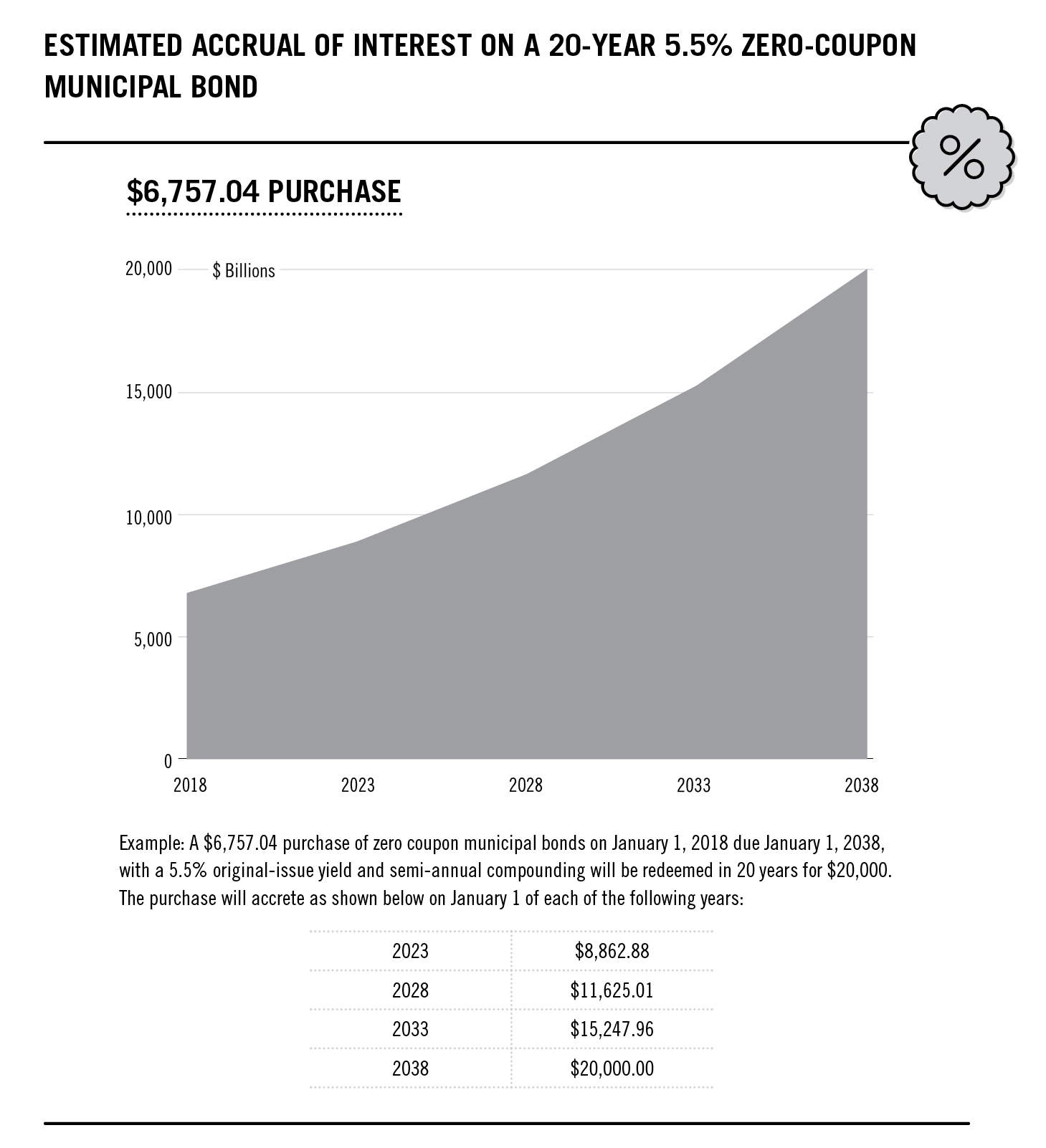

Investor's Guide to Zero-Coupon Municipal Bonds | Project ...

Solved a. What is the duration of a zero-coupon bond that ...

Duration Analysis

Portfolio Duration and its Limitations | CFA Level 1 ...

Zero Coupon Bonds Explained (With Examples) - Fervent ...

Bond Price Volatility Zvi Wiener Based on Chapter 4 in ...

Invest in Zero Coupon Bond at Yubi | Learn All About It

Aha! Interest rates do matter.

How to Calculate a Zero Coupon Bond Price | Double Entry ...

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

A 12.75-year maturity zero-coupon bond selling at a yield to ...

Post a Comment for "40 duration for zero coupon bond"